Business

MACROECONOMIC SCENARIO

With the exception of the United States, whose economy grew 2.4% in 2014, driving up the dollar, the world’s ten leading economies closed the year with slow growth or even in recession, according to the World Bank. In second place on the list, China registered its lowest growth since 1990. Japan, third on the list, ended 2014 in recession.

In Brazil, the scenario was no different. Gross Domestic Product (GDP) grew a meager 0.1%, according to the Brazilian Institute of Geography and Statistics (IBGE). GDP per capita fell for the first time since 2009, down 0.7%. The country closed 2014 with inflation of 6.41%, at the top end of the government’s target range, mainly driven by food and housing prices. Lack of rain also contributed to rising inflation, compromising farm productivity and reducing food supply.

Brazilian GDP grouwth (%)

The US$ 3.93 billion trade deficit in 2014 was the first annual negative balance since 2000 and the worst result since 1998 (-US$ 6.623 billion). While imports totaled US$ 229 billion in the

12-month period in 2014, exports came to approximately US$ 225 billion. The Ministry of Development, Industry and Foreign Trade (MDIC) justified the deficit by citing falling commodity prices, particularly for iron ore, the economic crisis in Argentina, one of the main importers of Brazilian products, and the increased spending on fuel imports.

Industrial production also fell by 3.2% in comparison with 2013 – the worst performance by Brazil since 2009, at the peak of the global economic crisis. Public sector accounts closed with a primary deficit of R$ 32.5 billion, the first time in Central Bank history.

A study on competitiveness conducted by the National Confederation of Industry (CNI) revealed that, despite slight gains in labor availability and costs, the weight of taxes and microeconomic factors, the country fell behind in terms of infrastructure and macroeconomic factors and continued in the penultimate position in the competitiveness ranking. The final position in the ranking is held by Argentina.

For more information on the performance and history of Triunfo’s operating sectors, please see page Triunfo.

OPERATING PERFORMANCE

In 2014, Triunfo maintained its excellent business performance, delivering positive results in the face of difficulties imposed by both the Brazilian and global economies. Learn more about the performance of Triunfo companies in each operating segment.

Toll roads

The toll roads business, which had three companies in its portfolio, gained strength in 2014 with the operational start-up of Triunfo Concebra. In September 2014 the company began providing emergency medical response and mechanical assistance services on a 1,176.5 km stretch of the BRs 060, 153 and 262 highways between the Federal District, Goiás and Minas Gerais. The company should begin charging tolls in the second half of 2015.

Another important operation, in 2014, was the progress made in the acquisition of the

321.6-kilometer stretch of BR-153 in the state of São Paulo. Managed by Triunfo Transbrasiliana, the stretch forms an important highway corridor, integrating the Triunfo Concebra and Triunfo Econorte concessions. The concession, which started in February 2008, is for 25 years.

Triunfo companies operating in the toll roads segment saw a 1.2% increase in vehicle equivalent traffic over 2013. The top performer was Triunfo Concepa, operating in Rio Grande do Sul, which recorded a 6% increase in traffic and 10% increase in average toll. In 2014, the company began investments approved under the contractual amendment signed with the ANTT. The agreement envisages the construction of the fourth lane on both directions of the BR-290/RS highway to improve access to Porto Alegre, the state capital.

Triunfo Concer, located in the state of Rio de Janeiro, moved one of its toll plazas on BR-040 from kilometer 104 to kilometer 102. As a result of this change, vehicles proceeding to the Rio de Janeiro metropolitan beltway no longer pass through the toll plaza, adversely affecting traffic volume. The company already factored in this loss of traffic (-3.2%) and to maintain the equilibrium of the concession agreement, an amendment was signed in August which passed on the effects of this loss to the toll, which was increased by 12.5%. The second portion of the increase will be applied in the 2015 toll revision, thus offsetting the entire traffic loss caused by the change in infrastructure.

On another front, the company restated in 2014, through an amendment signed with ANTT, the amounts stipulated in the original agreement for construction of the Nova Subida da Serra uphill lane on BR-040. Improvements include the construction of the largest highway tunnel in Brazil, spanning five kilometers.

Triunfo Econorte, headquartered in Paraná, saw a slight 1.4% decrease in traffic volume. Falling agricultural production due to drought had an impact on highway traffic. In December 2014, the company signed an amendment to the concession agreement, by which the Highways Department (DER) authorized an 8.25% increase in tolls, which were applied at the end of 2014. Average toll increase during the year stood at 13.1%.

Traffic

(in thousands of vehicle equivalents)

Effective average toll in the segment increased 11.1%, from R$ 7.82 in 2013 to R$ 8.69 in 2014.

Energy

The highlight in the power generation segment was the acquisition of the Três Irmãos Hydroelectric Plant, located in Andradina (SP) and controlled by Tijoá Participações e Investimentos S.A., which added value to the Company’s sales portfolio. In October 2014, Tijoá received its environmental operating license and will manage the plant for the next 30 years. The project, with installed capacity of 807.5 MW, joins the Garibaldi Hydroelectric Plant in Santa Catarina – operating commercially since 2013 – and the Salto Hydroelectric Plant, located in Goiás.

Under the management of Triunfo Rio Canoas, the Garibaldi Hydroelectric Plant has installed capacity of 191.9 MW, generating assured energy of 83.1 MWh, which corresponds to

727,956 MWh/year. Of the total assured energy, 70% was sold at an auction at the time, at

R$ 107.98/MWh. Adjusting for inflation by the Extended Consumer Price Index (IPCA), the price at the end of 2014 came to R$ 136.68/MWh. The remaining 30% of assured energy was sold on the free market at R$ 365.00/MWh in 2015 and R$ 250.00/MWh in 2016.

In 2014, the Garibaldi Hydroelectric Plant generated a total of 901,319.79 MWh. The strategy of advancing operational start-up by 13 months to take advantage of high energy prices brought successful results: excellent performance, driven by the first quarter, led to a 158% increase in assured energy sales at the end of 2014. EU1 EU2

Triunfo Rio Verde manages the Salto Hydroelectric Power Plant in Goiás, which has been operating since May 2010 with an installed capacity of 116 MW and assured energy of 67.8 MWh, which corresponds to 593,928 MWh per year. In June 2007, the Triunfo Rio Verde signed an agreement to sell 100% of the assured energy to Votorantim Comercializadora de Energia Ltda. (Votener). The agreement, valid for 16 years, was signed for an average price of R$130/MWh. The price, annually adjusted based on the General Market Price Index (IGP-M), reached R$ 201.83 at the close of 2014. The Transmission System Usage Tariff (TUST) is also reimbursed by Votener. In 2014, the net energy generated by the plant totaled

574,419.74 MWh. EU1 EU2

Assured energy sold

(thousand MWh)

Both Triunfo Rio Canoas and Triunfo Rio Verde were held for sale on December 31, 2014.

Energy - Effective average tariff

(R$/MWh)

Ports

The volume of TEUs handled by Portonave decreased slightly in 2014, by 0.8%. This number followed the Brazilian trade balance, which ended the year with a deficit of US$ 3.93 billion – the first negative result since 2000 and the worst since 1998. Apart from macroeconomic impacts, rains in June significantly affected – though on a non-recurring basis – operations at the terminal, which was closed for nine days and during which the stopover of five ships was canceled.

TEUs handled

|

In the month following the rainy period, Portonave began expansion work on the Navegantes Port Terminal, which will practically double its static capacity from 15,000 to 30,000 TEUs. The expansion should be concluded by the end of 2015 at an investment of approximately R$ 120 million. The yard, located on the right side of the Terminal, will be expanded from the current 270,000 m² to around 400,000 m² when construction work is concluded.

In 2014, Portonave also set the record for productivity in South America. Using six portainer cranes, the company set the record of 270.4 TEUs handled per hour while serving the vessel MSC Agrigento. In all, the company moved 2,064 TEUs in 7 hours and 38 hours of work, averaging 45 TEUs per crane.

Since 2009, Portonave has been the leader in container handling among port terminals in Santa Catarina. In 2014, its share of the state market was 44.5%, which reflects the competence of its professionals and the quality of services provided, considering that Santa Catarina has five highly competitive ports. |

In addition to its leadership in the state, in 2014 the Terminal remained the vice leader in market share in southern Brazil, accounting for 23% of all containers handled, only behind the Port of Paranaguá in Paraná.

Portonave - Effective average tariff

(R$/TEU)

Airports

Aeroportos Brasil Viracopos began operations in October 2014 at the new passenger terminal at the Viracopos International Airport. With investments of R$ 3 billion going into it, the new terminal offers 28 gates, 72 aircraft parking spots, three new aircraft tarmacs and a parking lot for 4 thousand cars. Driven by the World Cup in Brazil, the new terminal received

51.96 thousand passengers in 2014.

Traffic at the Viracopos International Airport

Flights are gradually being transferred to the new terminal, a process that should be completed during 2015. The number of international flights per week increased from three to 38. The beginning of operations at the New Terminal and the airport’s efficiency during the World Cup (more information on page Triunfo) contributed to an increase of 552 thousand in passenger traffic at the terminal compared to 2013, up 5.9%.

Distribution of passengers

Viracopos International Airport

Aircraft traffic also increased by 3.3% over 2013. Only cargo handling decreased, falling 7.5%. The decrease in cargo volume was not restricted to the Viracopos International Airport, but was the result of worsening trade deficit and declining industrial production in Brazil.

ECONOMIC AND FINANCIAL PERFORMANCE

Since January 1, 2013, with the compulsory application of IFRS 10 and 11, and CPC 36, Triunfo ceased to proportionally consolidate its jointly controlled subsidiaries (Concer, Portonave and Aeroportos Brasil Viracopos) in the financial statements. As such, the results of Concer have since been consolidated in full, while the results of Portonave and Aeroportos Brasil Viracopos are recorded under “Equity Income”. In the financial statements for fiscal year 2014, the subsidiaries Maestra, NTL and Vessel ceased to be segregated among “Assets and Liabilities of Discontinued Operations” and their results were once again included in the Company’s consolidated financial statements.

Triunfo believes that the proportional consolidation of operations better reflects its cash flows and hence this chapter of the report provides financial information in proportion to Triunfo’s interest in each company, whereas operating data consider 100% of each business. The report includes the performance of Triunfo Rio Verde and Triunfo Rio Canoas – which, in the financial statements, were classified as “Operations held for sale.”

In 2014, consolidated gross revenue of Triunfo companies reached R$ 2,581.1 million, representing growth of 15.5% from the previous year. Adjusted net revenue, which excludes revenue from the construction of concession assets, totaled R$ 1.3 billion, increasing 36.7% from 2013. The increase in adjusted net revenue and adjusted EBITDA (85.9%, with margin of 73.8%) underlines the cash generation capacity of Triunfo’s assets. G4-9

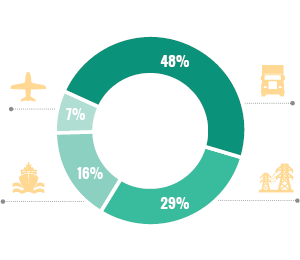

Breakdown of Net Revenue in 2014

|

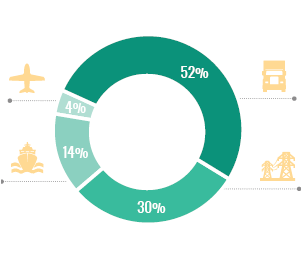

Breakdown of adjusted Ebitda in 2014

|

Evolution of Net Revenue and Ebitda

(R$ million)

At the close of 2014, Triunfo’s consolidated cash cost was R$ 305 million, up 12.7% from 2013. Cash expenses reached US$ 156.4 million, increasing 38.7% from the previous year. The main reasons behind this increase include increased power generation costs and expansion of staff strength to meet business expansion.

The 2014 results were significantly impacted by the discontinuation of Vetria Mineração, due to the recognition of impairment of its assets. Triunfo recorded the effect of R$ 614.7 million, whereas the consolidated effect was R$ 597.5 million under expenses and R$ 17.2 million under equity income (loss). Of the total impact, R$ 481 million was supported by unrealized profits reserve and hence does not affect the dividend calculation base. Note that this is only an accounting effect, with no cash impact.

As such, the dividend calculation base was R$ 107.2 million in the 12-month period of 2014, reflecting the solid consolidated operating performance.

Triunfo suspended its cabotage operations at the end of 2013. On December 31, 2014, the subsidiaries Maestra, NTL and Vessel ceased to be segregated between “Assets and Liabilities from Discontinued Operations” and their results were once again included in the Company’s consolidated financial statements. The change in consolidation is due to the fact that Maestra, NTL and Vessel started a new operating cycle with the focus on providing highway services.

Generation and distribution of wealth

Toll roads

Adjusted net revenue from the segment was R$ 622.6 million (+23.9%) in 2014. Increased tolls contributed to improved revenue from toll collections in this segment, which reached

R$ 601.3 million in 2014, an 8.9% increase over 2013.

Toll increases saw real gains throughout 2014 and nullified the negative impact of slower volume growth in the segment. In 2014, the toll increases were: (i) 12.5% at Concer; (ii) 10% at Triunfo Concepa; and (iii) 13.1% at Triunfo Econorte.

Energy

Adjusted net revenue from the segment reached R$ 387.4 million in 2014, of which

R$ 129.4 million came from Triunfo Rio Verde, R$ 277.2 million from Triunfo Rio Canoas and

R$ 10.9 million from Tijoá, which began operating in October. This result was a 151.9% increase from the segment’s results in 2013.

Operating costs and expenses also increased in the period – by 143.3% and 119.4%, respectively. The full operational start-up of the Garibaldi Plant, together with the operational start-up of the Três Irmãos Plant, contributed to a part of this increase. Furthermore, costs resulting from the average reduction of 15.13% in assured energy from the system required the company to purchase 15,670.504 MWh to meet contractual requirements in the fourth quarter of 2014.

Ports

Reflecting the decrease in TEUs handled during the year, net revenue from the port segment in 2014 fell 4%. Offsetting the negative effect of reduced handling, Portonave registered an important increase in revenue from yard services, such as container storage, which reached

R$ 135.3 million in 2014, up 32.2% from 2013.

Investments in expansion by Portonave, as well as hiring and training of professionals to operate new equipment, contributed to the increase in operating expenses (excluding depreciation and amortization), which came to R$ 69 million in 2014 (164% increase over the previous year). Operating costs, in turn, fell 36.5%, reaching about R$ 58.2 million at the end of the year.

Airports

Adjusted net revenue from the segment was R$ 91.7 million in 2014, up 10.3% from the previous year. Passenger revenue – from departures, arrivals, connections, take-offs and landings – increased 8.4% from 2013, totaling R$ 26.3 million.

During the year, cargo volume fell 7.5%, while revenue from this niche increased 5.8% to

R$ 64.4 million. This result was due to the actions taken by Aeroportos Brasil Viracopos to attract high-value cargo, attract and foster loyalty among pharmaceutical and chemical companies, improve infrastructure and reduce the average time for cargo clearance.

Airport operating costs fell slightly in the period: 2.1%. Expenses increased 21.4% in comparison with 2013, mainly due to the hiring of professionals to operate the new passenger terminal.

Share performance

In 2014, Triunfo stock depreciated 18.9% to end the year at R$ 7.70, while the Ibovespa, the main index of the BM&FBovespa, dropped 2.9%. Average financial trading volume per day of Triunfo stock reached R$ 987,000 in 2014, up 215.3% from 2008, the first year the stock was traded since the IPO.

Stock performance – Triunfo x Ibovespa

(Base 100)

© 2015 Relatório de Sustentabilidade

© 2015 Relatório de Sustentabilidade